The Problem: Interest Rates are going up

The 30-year fixed mortgage interest rate increased nationally from 6.33% to 6.4% this week while the 5/1 adjustable rate mortgage also increased from 5.93% to 6.01%. In New Jersey, the numbers are a bit higher but the rate actually fell from 6.44% to 6.42%.

The federal fund rate increased slightly over the last three months. The federal fund rate (FFR), which is the interest rate banks with excess reserves at a federal-reserve district bank charges member banks needing overnight loans to meet reserve requirements, is the most sensitive indicator of interest rates because it is set daily by the market. It is more sensitive than the prime rate which is set by banks or the discount rate which is set by the Fed.

Why it Matters to YouThe rate increasing means an average buyer will get less house for his or her investment dollar since more will go to repaying the interest on the mortgage. It makes sense to pay more during the early few years of the mortgage to pay down the principle so that the amount paid toward the end of the mortgage will decrease.

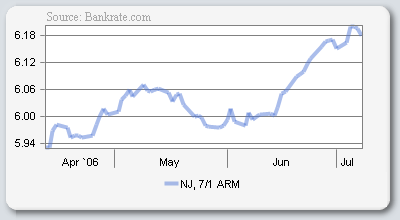

For those whose credit history is relatively small or those with poor credit the outlook is less promising. Often these buyers are ineligible for fix rate mortgages. The 7/1 adjustable rate mortgage (ARM) rate in New Jersey though lower than the 30-year fixed rate at 6.18% dropped from last week’s 6.2%.

Unfortunately, a 7/1 ARM means after the first seven years of the mortgage, the rate can change annually. Many people are finding themselves facing foreclosure with ARM payments becoming too high for their income. According to Foreclosure.com foreclosures are expected to rise across the country. An article appearing in the business section of Colorado's Pueblo Chieftain describes the situation of one family. The falling unemployment rate has helped keep more people from falling behind in the first three month of this year but it is a delicate balance. Any rise in the unemployment rate and the expected rise in the foreclosure rate may almost be a certainty.

What is HappeningBuyers are not the only one taking a second look at things. Builders are also re-evaluating their perspectives on the new-home market as are their investors. The sellers market of 2005 has changed. What the new-home market can tolerate is still unclear but builder confidence is decreasing according to the National Association of Home Builders/Wells Fargo Housing Market Index (HMI) for June. From a May report to the June report the index for the Northeast fell seven points.

What the rising interest rate means to the house seller is that it will take longer to find a buyer. If the house seller is using the sale of their present home to purchase their new home getting the timing synchronized will be essential. Pre-qualifying for mortgages will help determine the amount of house a buyer can afford. The best place to find a person with the most experience of pointing people in the right direction for a mortgage broker is the professional realtor. Still mortgage brokers are not hard to find.

What You Can Do

Everyone involved in the housing market is affected either directly or indirectly by the changes in the interest rate and everyone needs to pay attention. The housing market is directly impacted by the unemployment rate. So a rise in it will affect the housing market. Hopefully the American economy will stabilize and her people will remain employed. We all need to just keep an alert eye on things.

Technorati: NJ Real Estate News, Real Estate, NJ Real Estate Blogs, NJ Housing, New Jersey

No comments:

Post a Comment